ServiceNow profits when Microsoft wins

A structural analysis of who owns the control plane in enterprise AI

Disclosure: The author holds a long position in ServiceNow (NOW). This analysis was conducted before the position was established and reflects the structural reasoning behind it.

There is a company that figured out how to make money from Microsoft and Salesforce winning the AI race. It is neither Microsoft nor Salesforce.

Last year ServiceNow launched something called AI Control Tower. It looked like another enterprise management tool. It is not. It is a governance layer for every AI agent operating inside an organization, including agents built by competitors. An enterprise running Microsoft Agent 365 uses ServiceNow to decide what those agents are permitted to touch, which systems they can access, and when they must escalate to a human. Every new agent deployed, regardless of vendor, becomes another reason to keep the ServiceNow contract.

The market knows ServiceNow is a good company. What it has missed is that the mechanism driving the company’s structural value gets stronger as competitors win, not weaker.

Why agents need a foundation

An AI agent resolving an IT incident is not a chatbot. It needs to know what broke, how the systems connect, what is safe to change, and when to stop. None of that lives in the AI model. It lives in the CMDB, the Configuration Management Database that has been the backbone of ServiceNow’s platform since 2004.

CMDB is not a database in any conventional sense. It is a live register of every asset, dependency, and change in an organization’s technology environment. Every IT process in a large enterprise is built on top of it. Replacing it means rewriting that process logic from scratch, a project that takes years and costs more than the license fee. That is why 98 percent of ServiceNow’s customers renew. Not loyalty to a product. Architectural lock-in with no easy exit.

When AI agents arrived, they needed exactly what CMDB already held. ServiceNow did not build this position for the AI era. It built it in 2004, and the AI era walked straight into it.

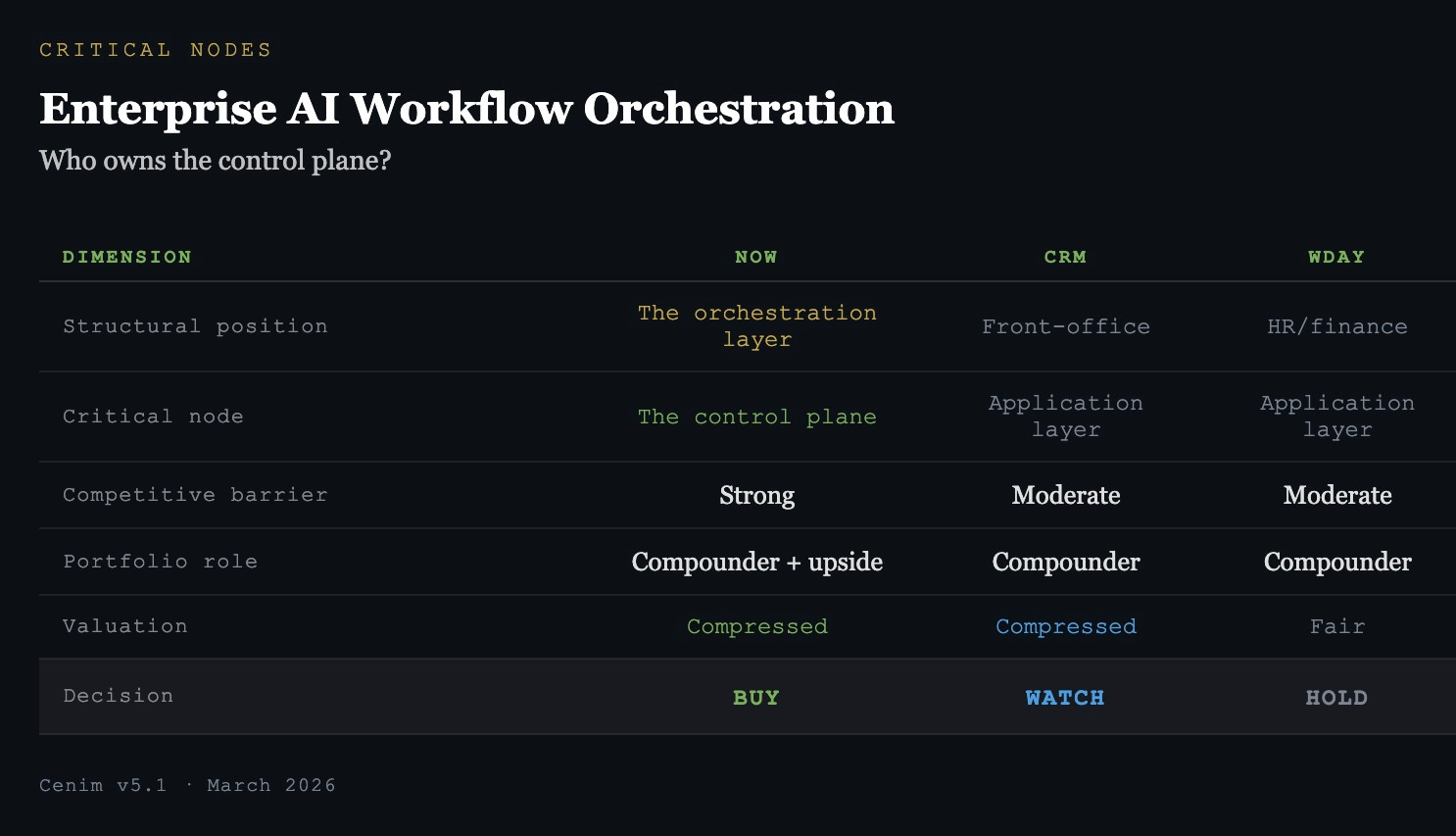

Not the same market

Salesforce and Workday appear regularly in the same sentence as ServiceNow. The comparison is wrong. They sit in different layers of the stack and hold fundamentally different structural positions.

Salesforce owns the front office. Agentforce handles customer interaction, sales, service cases, and it is growing fast. Nearly 800 million dollars in ARR last fiscal year across 150,000-plus customers. But front-office agents do not touch production infrastructure. They do not rewrite network configurations or provision servers. The layer that governs whether an agent can do that is ServiceNow’s layer, and Salesforce does not compete for it.

The monetization gap is worth pausing on. ServiceNow crossed 600 million dollars in Now Assist ACV against 7,700 enterprise customers. Salesforce’s 800 million dollars is spread across an install base twenty times larger. The revenue per customer comparison does not favor Salesforce.

Workday runs HR and finance applications. 1.7 billion AI actions on the platform last fiscal year is a real number. But those actions automate processes within Workday. They do not orchestrate agents across an enterprise’s entire technology environment. Workday competes in the application layer. The orchestration layer is a different address.

What the selloff actually reflects

NOW has fallen 30 to 50 percent from its peak. The cause is a category-wide sentiment shift against SaaS, not anything that has happened to ServiceNow’s business. Subscription revenue grew 21 percent organically last year. Gross margin held at 77.5 percent. cRPO, the forward revenue contracted but not yet recognized, stood at 12.85 billion dollars at the last report, up 25 percent year over year. The company reached 1, 5, and 10 billion dollars in revenue without a meaningful acquisition. That organic growth trajectory has no close parallel in enterprise software history.

The stock trades today at roughly 8 to 9 times EV/Revenue, approximately half of historical normal for this business. Thirty-one analysts cover it. The consensus is Strong Buy, average price target near 203 dollars against a current price around 114 dollars after the December 5-for-1 split.

A company with 77 percent gross margins, 20 percent organic growth, and a structural position that compounds as the broader market expands does not become a bad investment because SaaS fell out of favor. It becomes cheaper.

Two risks worth tracking

Microsoft is currently a partner. Agent 365 integrates with AI Control Tower. But Microsoft has both the capability and the incentive to build orchestration directly into Azure if they choose to, cutting ServiceNow out of the governance layer entirely. There is no signal that this is coming. Given ServiceNow’s penetration across 85 percent of the Fortune 500, it would be a costly move to make. But it is the only competitive threat that actually matters, and it deserves a quarterly check.

The longer-horizon risk is architectural. If agentic AI eventually enables agents to coordinate directly without a platform intermediary, the orchestration layer loses its structural necessity. That is unlikely within five years. It is not impossible within ten. It belongs in the thesis as a monitoring condition, not as a reason to avoid the position today.

The quiet part

The investment narrative around ServiceNow focuses on Now Assist growth, on the race to a billion dollars in AI ACV, on how the numbers compare to Salesforce quarter by quarter. Those are the right questions for a trading thesis. They are the wrong questions for understanding where the structural position is going.

The moat does not grow because the product improves. It grows because every agent deployed in an enterprise environment, by any vendor, creates another dependency on the foundation that agent must stand on. That mechanism compounds with the scale of the system it sits inside. It operated before the AI narrative existed. It will operate after the narrative moves on.

ServiceNow built the control plane in 2004. The rest of the industry spent twenty years building things that need it.

This analysis is based on Cenim v5.1, a structural investment framework for technology systems. Nothing in this article should be read as financial advice.